- Nearly 48% of older adults carry a credit card balance from month to month, with 20% relying on credit for essential expenses.

- Rising cost of living and inflation have made it harder for retirees to cover everyday expenses, worsening financial insecurity.

- Healthcare costs, especially dental and prescription expenses, are a major contributor to credit card debt for older Americans.

- Fixed incomes make it difficult for retirees to pay off debt, with 43% concerned about their repayment timeline and many taking over five years to become debt-free.

- Home equity can provide financial relief, with strategies like downsizing, home equity loans, and reverse mortgages helping retirees reduce debt burdens.

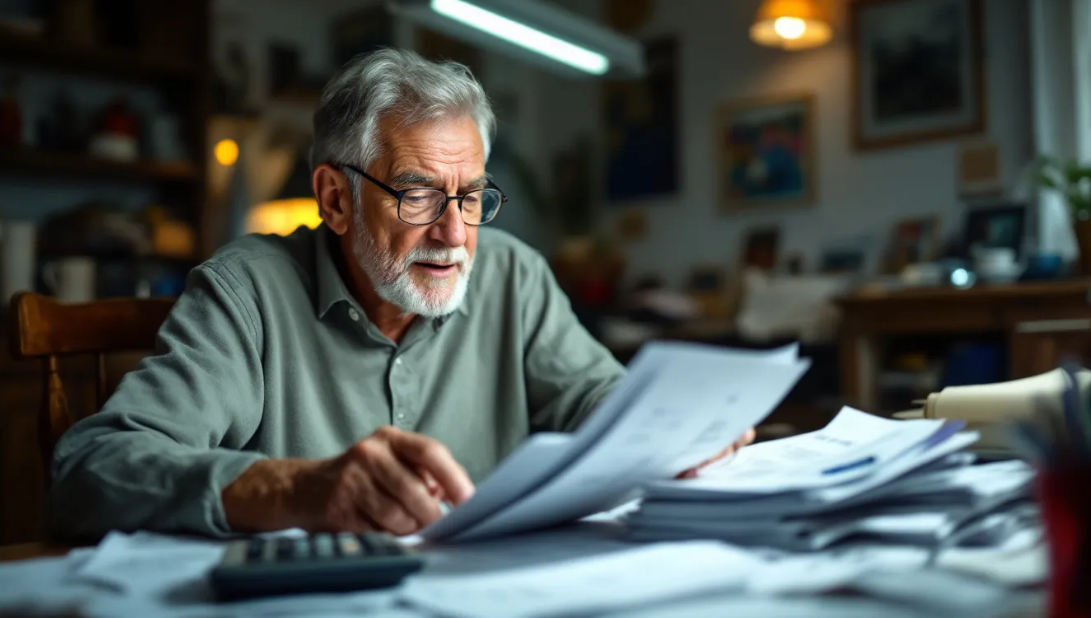

More older Americans are turning to credit cards to cover essential expenses, a trend that threatens their financial security in retirement. Rising costs for housing, healthcare, and daily necessities have led many retirees and pre-retirees to carry significant credit card debt. With fixed incomes and limited financial flexibility, this growing dependence on high-interest debt is creating long-term financial strain. However, real estate assets, such as home equity, may offer a solution to ease this burden.

The Growing Dependence on Credit Cards

Credit card debt is becoming a major financial challenge for older Americans. The recent AARP survey highlights alarming trends in debt accumulation among retirees:

- 48% of older adults carry a credit card balance each month.

- 20% use credit cards regularly to cover basic expenses like food, rent, and utilities.

- 37% reported having more debt than the previous year, indicating a worsening financial trend.

- 28% of those in debt owe $10,000 or more—a significant amount given that many are on fixed incomes.

With rising costs making everyday expenses harder to manage, credit cards become a quick but costly solution. Unfortunately, high interest rates can trap retirees in a cycle of debt that is difficult to break.

Rising Cost of Living and Its Impact

Inflation and the rising cost of living are placing greater financial strain on retirees. Many older Americans depend on Social Security, pensions, or retirement savings, but these income sources have not kept pace with inflation. Essentials such as groceries, utilities, transportation, and home maintenance have increased in price, leading many to rely on credit cards to make ends meet.

The impact of rising housing costs is particularly significant. Property taxes, homeowners insurance, utilities, and rent continue to rise, leaving many financially stretched. Fixed incomes that once provided a comfortable retirement are now insufficient, pushing many retirees into debt to cover the basics.

Healthcare Costs as a Major Burden

Healthcare expenses are one of the biggest contributors to financial strain among older adults. The AARP survey revealed that 50% of respondents attributed their credit card debt to healthcare costs. Some of the most common medical expenses driving debt include:

- Dental care (46%) – Many Medicare plans do not cover dental procedures, leaving retirees to pay out of pocket for care like crowns, implants, or routine cleanings.

- Prescription medications (35%) – Even with Medicare Part D, many seniors face high out-of-pocket costs for necessary medications.

- Vision care (19%) – Coverage for eye exams, glasses, and treatments for conditions like cataracts is often limited, forcing retirees to turn to credit cards.

With healthcare costs continuing to rise, these expenses often feel unavoidable. Older adults may delay medical care due to financial concerns, which can lead to more significant health problems and even higher costs in the future.

Fixed Incomes and Financial Struggles

Living on a fixed income presents financial challenges, especially when costs rise without a corresponding increase in income. Retirees who struggle with debt often have fewer opportunities to earn additional income, making it difficult to escape the weight of high-interest credit card balances.

According to the AARP study:

- 43% of retirees with credit card debt are concerned about how long it will take to pay it off.

- 1 in 5 expect it will take over five years to be debt-free, significantly affecting retirement financial security.

The longer it takes to pay off debt, the more interest accumulates, making the problem worse over time. Those without emergency savings may find themselves stuck without a financial safety net when unexpected expenses arise.

Housing Costs and Financial Pressure

Housing is one of the largest expenses for older Americans, and rising costs are adding to their financial stress. Whether they rent or own a home, retirees face increasing property-related expenses:

- Homeowners may struggle with property taxes, maintenance, and insurance costs. Unexpected repairs like a broken HVAC system or roof replacement can quickly deplete savings.

- Renters face rising rents, with limited options to reduce costs, particularly in competitive housing markets where fixed-income retirees may find affordable housing harder to secure.

These expenses often force retirees to dip into savings, rely on credit cards, or downsize to a more affordable living situation.

The Role of Real Estate in Financial Stability

For older homeowners, real estate can be a vital financial tool in managing debt and improving financial security. Home equity, the value of a home minus mortgage debt, offers several potential strategies to alleviate financial pressure:

- Downsizing – Selling a larger home in favor of a smaller, more affordable one can reduce maintenance costs, utility bills, and property taxes while freeing up cash.

- Home Equity Loans or HELOCs – Both options allow homeowners to borrow against their home’s equity, typically at much lower interest rates than credit cards, to consolidate and manage debt more effectively.

- Reverse Mortgages – Available to homeowners aged 62 and older, a reverse mortgage provides monthly cash payments based on home equity, helping retirees cover living expenses while staying in their home.

For many retirees, leveraging home equity can provide a much-needed financial cushion to reduce reliance on credit cards while preserving long-term financial security.

Alternatives to Credit Card Debt for Older Adults

Beyond real estate solutions, older Americans can explore other financial strategies to manage debt and avoid excessive credit card use:

- Budgeting and Expense Management – Tracking spending, cutting unnecessary expenses, and prioritizing essential costs can reduce financial strain.

- Low-Interest Loan Options – Personal loans or refinancing options may offer lower-interest alternatives to credit cards, helping retirees manage debt more efficiently.

- Retirement Fund Withdrawal Strategies – Seeking professional financial advice to develop a strategic withdrawal plan can ensure retirees make the most of their available resources without accumulating high-interest debt.

Long-Term Consequences of Carrying Debt in Retirement

Carrying significant credit card debt in retirement can have severe financial and emotional consequences:

- Increased stress and anxiety about financial security.

- Reduced quality of life, as more income goes toward debt repayment rather than enjoying retirement.

- Risk of delaying healthcare due to financial concerns, leading to worse health outcomes.

- Potential depletion of retirement savings, leaving retirees financially vulnerable in later years.

Addressing debt proactively by exploring alternatives and seeking professional financial advice can help prevent these challenges and create a more stable retirement.

The Importance of Financial Planning for Aging Americans

To maintain financial security, older Americans should engage in proactive financial planning. This includes:

- Reviewing retirement savings and creating a sustainable withdrawal strategy.

- Exploring debt management solutions, such as credit counseling or refinancing options.

- Considering real estate options, like downsizing or leveraging home equity, to improve financial flexibility.

For homeowners, meeting with a trusted real estate expert can provide insights into how home equity can improve financial stability. By making informed financial decisions early, retirees can reduce financial stress and enjoy a more secure and comfortable retirement.

Local Considerations for Las Vegas Retirees

For retirees in Las Vegas, understanding the rising cost of living compared to national trends is essential. Housing costs, taxes, and rental rates in metropolitan areas may push some retirees to consider downsizing or relocating. Fortunately, Las Vegas offers real estate opportunities that can help retirees reduce expenses and improve financial security.

Consulting an experienced real estate professional like Steve Hawks can help older homeowners evaluate their options, from selling their home to leveraging home equity, ensuring they make the best financial decisions for retirement security.

Citations

AARP. (2024). Survey on credit card debt among older adults. Retrieved from https://www.aarp.org/pri/topics/work-finances-retirement/financial-security-retirement/credit-card-debt-survey/