- Over 30% of declined mortgage applications are due to high debt-to-income (DTI) ratios.

- FHA loans can serve as fallback options when credit scores drop below conventional loan limits.

- Gift funds and co-signers are top fixes when buyers fall short on down payments.

- Appraisal discrepancies can often be bridged through strategic negotiations or seller assistance.

- Buyers with contingent offers are most vulnerable to deal failure if their current home doesn’t sell.

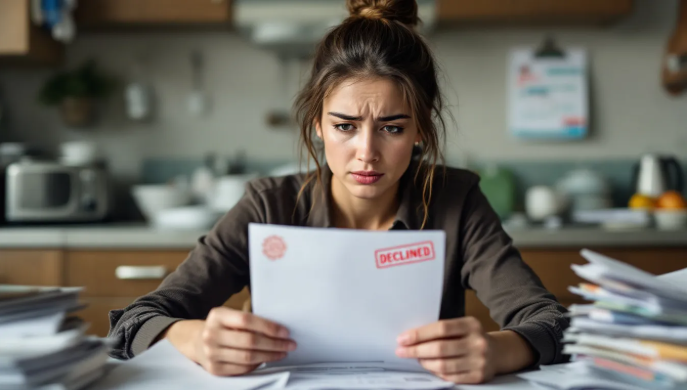

You just received the news—financing denied. The buyer’s loan did not go through, and now your deal is in a precarious position… or is it? Do not be alarmed. This is not necessarily the end. Actually, many real estate transactions can still be rescued if prompt, appropriate actions are taken. Drawing from the insights of Las Vegas expert Steve Hawks, who has successfully closed over 4,000 deals, this guide will demonstrate how real estate professionals like you can convert a financing problem into a closed transaction.

Why Home Loan Rejections Happen

It is important to first understand the reasons for a mortgage rejection to find an effective solution. Without identifying the core issue, buyers, agents, and sellers might waste valuable time and resources pursuing incorrect remedies. Home loans can be denied for many different reasons, but some issues are more frequent than others.

Common Causes of Loan Denial

- Insufficient down payment or high closing costs: Buyers often do not realize the total amount of funds needed at closing, especially when considering taxes, fees, and earnest money.

- Debt-to-Income (DTI) ratio exceeds lender limits: A buyer who is otherwise financially sound might have too many current debts, making the requested mortgage seem unaffordable on paper.

- Low credit score or negative credit history: Defaults, collections, liens, or even high credit usage can drop buyers below the required lending score.

- Sale of current home falls through: For buyers with contingencies, losing the funds from a home they were selling can completely eliminate their buying ability.

According to the Fair Credit Reporting Act (FCRA), lenders must provide the reasons for loan denial in writing. Agents might not have direct access to this information because of privacy regulations, but it is vital to encourage buyers to ask for and share their rejection letter. This information is key to creating the correct recovery plan.

Step One: Pause, Communicate, and Extend

When a buyer’s loan is denied, the initial reaction might be to panic or immediately switch to a backup offer. However, experienced agents understand that many real estate financing problems are temporary and can be fixed.

Key First Moves

- Request a short contract extension (7–14 days) — This allows needed time to troubleshoot or change lenders.

- Keep all parties informed — Open communication among buyer, seller, co-agents, and mortgage officers is crucial.

- Hold off on acting on backup offers too soon — Unless the current deal is truly over, stay focused on saving it.

According to Steve Hawks, many financing failures in Las Vegas were not due to unsolvable problems, but to missed or misunderstood rules in underwriting, miscommunications, or small missing documents that could be resolved quickly.

Fix #1: Down Payment and Closing Cost Issues

One of the most typical obstacles in real estate financing is not having enough liquid funds. Many buyers, specifically those buying for the first time, are unaware of the actual cash needed at closing, which can include prepaid taxes, insurance, appraisal costs, and HOA fees in addition to the down payment.

Easy Fixes

- Gift Funds: Loans backed by the government like FHA and VA often permit family members to gift money toward down payments or closing costs. Usually a properly documented gift letter and proof that the donor can provide the funds are sufficient.

- 401(k) Loans or Withdrawals: Buyers can borrow from their retirement funds to buy a home, often with minimal penalties if they pay it back quickly.

- Co-signers: Getting a relative or partner to co-sign not only adds financial security—it might also provide more down payment funds that qualify.

- Appraisal Gap Negotiations: If the buyer is struggling to cover a difference from a low appraisal, the seller could cover some or all of the difference or lower the home price.

Advanced Solutions

- Seller Second Mortgage: Also known as a carryback loan, the seller finances part of the purchase after the primary lender. This can lower the cash needed for closing.

- Raise Purchase Price to Cover Buyer Costs: If the appraised value supports it, the price increase can take care of the buyer’s costs through a seller credit, which is included in the mortgage.

- Temporary Seller Financing: For buyers who are financially stuck, short-term seller financing allows them to take possession while working to qualify for a refinance soon.

According to expert data, buyers frequently address funding gaps using gift funds, qualified withdrawals, or co-signers when standard funding is not possible.

Fix #2: Tackling Debt-to-Income Ratio (DTI) Issues

High DTI ratios are the main reason for home loan rejection. Even with a reliable income, large monthly debts can quickly disqualify a buyer.

Understanding DTI Thresholds

- Front-end DTI (Housing): Usually must be less than 28%

- Back-end DTI (Total Debt): Generally, cannot be more than 36% for most standard loans

If the buyer goes over these limits, lenders might withdraw their approval, but it is not hopeless.

How to Reduce DTI

- Pay Down Revolving or Installment Debt: Lowering or getting rid of monthly payments (for example, car loans or credit cards) can directly improve DTI.

- Switch to More Lenient Loan Types: FHA or VA loans can allow higher DTI ratios, and some specialized programs (like USDA) might also have less strict requirements.

- Increase Down Payment: By lowering the loan amount, some buyers can get their DTI under the approval limit.

- Use a Co-Signer or Income Earner: Adding another person’s income can reduce perceived risk and improve ratio balance.

Experts agree that rising interest rates and home prices have made DTI failures worse, and innovative debt arrangement is now more important than ever.

Fix #3: Credit Score Corrections

Credit scores change often and are very important factors in real estate financing approvals. Luckily, there are quick solutions that can improve a buyer’s file quickly.

General Credit Requirements

- Conventional Loans: Minimum score usually around 620

- FHA Loans: Typically allow scores as low as 580 with other positive factors

Fast Improvement Tips

- Experian Boost or Similar Programs: Adds positive payments that are not usually considered — like cell phone and utility bills — to raise scores.

- Dispute Inactive or Incorrect Items: Inaccurate information found on credit reports—especially older items—can be disputed and taken off in 48–72 hours in some situations.

- Reduce Credit Utilization: Paying off credit cards that are maxed out can sometimes raise scores by 15–50 points in a few days.

- Settle Public Records or Liens: Negotiating settlements on negative items—even before they are fully paid—can help with loan acceptance, especially if documented.

Even a score drop of just 15 points can change your borrower’s eligibility—but that drop can often be fixed in a few days.

Fix #4: Previous Home Sale Tanked

Buyers with contingent offers often need the money from selling their current home to qualify for the next one. If the first transaction fails, the second one often fails as well—unless something is done.

Deal-Saving Alternatives

- Shift to “Kick-Out Clause” Contingency: This allows sellers to continue marketing the home while giving the original buyer “first right of refusal” if another offer is made.

- Negotiate Time Extensions: A grace period of one to two weeks might be all that is needed to fix a failed chain reaction.

- Aggressive Relisting Strategy: Speed up the relisting of the first home using specific buyer groups or price changes.

Problems from failed home sales can be handled if everyone involved is open to timelines and temporary solutions.

Alternate Financing Options Worth Considering

When standard lending does not work, other strategies are available to bridge the gap between mortgage rejection and a successful closing.

Types of Alternative Financing

- Hard Money Lenders: Offer short-term loans backed by assets, which are good for buyers who need time to fix credit or income proof problems. They have high rates but very fast approval.

- Sell Leaseback Arrangements: If the seller has timing problems, a buyer may purchase and lease the home back to the seller, giving the seller time to move out while funding the buyer’s purchase.

- Piggyback Loans: Using a secondary loan (usually a HELOC or second mortgage) can lower the primary loan amount and improve loan-to-value (LTV) ratios.

Although not best for long-term financing, these solutions can rescue a deal that would otherwise fall apart.

Know the Legal Terrain

When quickly trying to save a deal that is falling apart, do not forget the legal and ethical duties related to real estate financing.

Best Practices to Stay Compliant

- Respect Privacy Laws: Buyers are protected by the FCRA and other laws that prevent sharing financial records without permission.

- Put Everything in Writing: All agreements, repairs, extensions, or financing changes must be written down properly and agreed to by both parties.

- Avoid Misrepresentation: Be careful not to exaggerate or guess about the reasons for financing denial. Only share confirmed facts.

Partner in the Process: Local Lending Insight

Steve Hawks emphasizes that in markets like Las Vegas, working with experienced, local loan officers can be the deciding factor between saving a deal and losing it.

Local Lender Advantages

- Accurate Appraisals: Local lenders understand home values in specific neighborhoods and are less likely to depend on inaccurate automated valuations.

- Faster Underwriting: National companies might take weeks; dedicated local firms often close in half the time.

- Understanding Unique Buyer Types: From casino employees to military personnel moving to the area, local details are important—and local lenders understand them.

Backup Offers: Proceed With Caution

It is tempting to quickly move to a backup offer when financing fails—but doing so too soon can cost money and damage relationships.

Ask These Before Proceeding

- Is the new buyer fully underwritten and approved?

- Can the current buyer solve their financing problem in just a few days?

- Would losing the original buyer’s offer reduce the seller’s net profit?

Unless the original buyer is completely unable to continue, it is often smarter—and faster—to fix their deal rather than start over.

Experts recommend using all options to fix the primary deal before activating backup buyers—especially if the original offer was better.

Your Role as an Agent: The Calm in the Storm

A licensed agent’s role is much more than just opening doors. When a deal is in danger, your attitude and decisions are extremely important.

How to Lead Buyers & Sellers Through Crisis

- Stay Objective & Rational: Your reaction sets the emotional tone for everyone involved.

- Facilitate, Don’t Dictate: Make connections, show options, help buyers choose—do not force decisions.

- Focus on Solutions: The best agents are known not for avoiding problems, but for finding creative solutions.

Vet Buyers Better—Avoid the Drama

It is better—and easier—to prevent problems than to fix them late in the process. Improve your screening processes for future deals.

Smart Vetting Strategies

- Require Full Pre-Approvals, not just pre-qualifications

- Request Proof of Reserves, Assets, and Credit Scores before accepting an offer

- Coordinate Early Communication with the Lender to understand risk factors

- Examine Buyer’s Timeline, Current Debts and possible problems early on

You’re a Deal Saver, Not Just a Door Opener

Getting to “under contract” is just the start. Turning “financing denied” into “deal saved” is what makes top agents stand out. When real estate financing fails, there are always options—but only if you know what to look for, act quickly, and bring the right people together.

With creativity, clarity, and confidence, you can guide buyers and sellers through difficult situations and achieve success. That is what makes you so valuable in every transaction.

Want expert guidance or direct support for your Las Vegas deals on life support? Connect with Steve Hawks today and turn “deal denied” into “deal done.”